Most articles about money journaling sound like recipes for guilt. Track expenses. Set goals. Clip coupons. Those are useful, but they are small levers on a complex machine. If you want something that actually changes your relationship with money, you need a practice that combines the precision of a lab notebook, the curiosity of a novelist, and the discipline of an athlete. That is why I propose an experimental approach to journaling for money that treats your financial life as a living system to observe, iterate, and redesign.

Before we begin, remember the title of this piece, Journaling for Financial Clarity: A Radical System for Money Mindset and Strategy. Read it now. The sentence is your north star. Throughout this article we will test, record, and revise. We will turn feelings into data and data into decisions, but we will not lose the texture of your life in the process.

Why this is not another budgeting article

Most money-writing applies a universal solution to individual problems. You get a spreadsheet and a moral pep talk. That rarely works long term because money behavior is anchored in identity, memory, and context. What transforms behavior is not just knowledge. It is sustained observation plus actionable experiments that are small, measurable, and humane.

To start, consider this meta rule: treat your journal as a research tool, not a confessional. Open the notebook to discover patterns, test interventions, and map trade offs. The goal is financial clarity, not perfection.

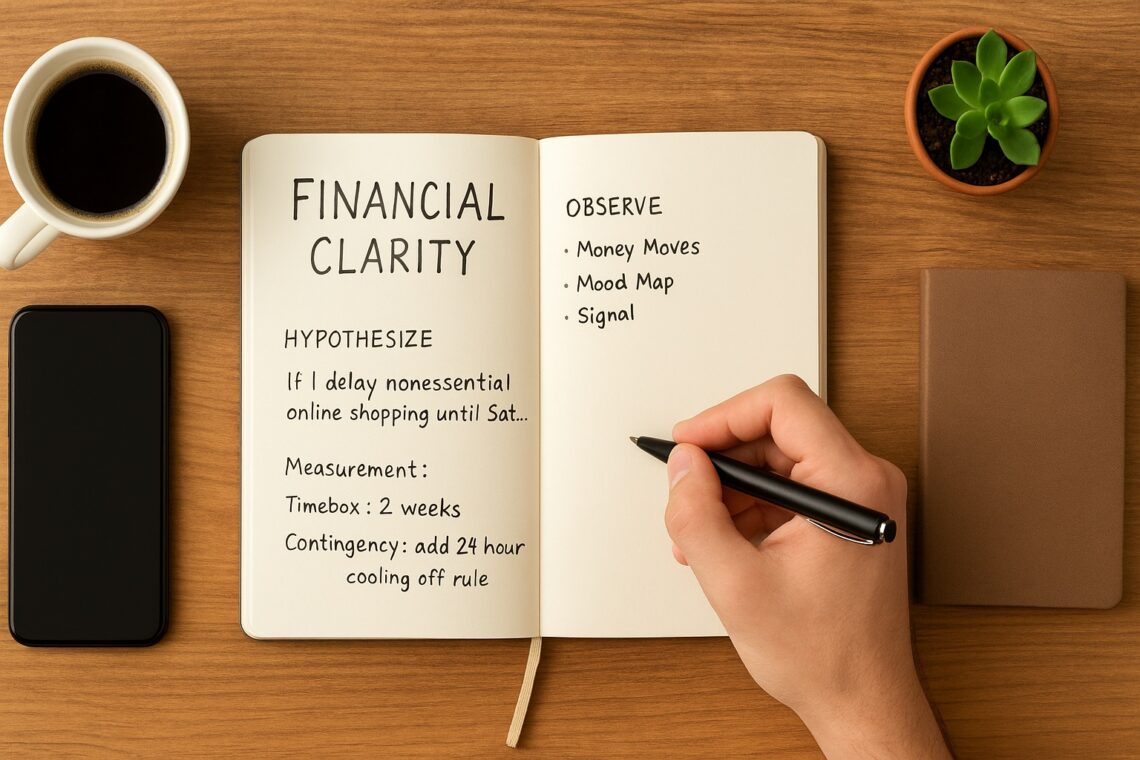

A three-part practice

This system has three parts: Observe, Hypothesize, and Iterate. Each part is short enough to do daily and rich enough to reward long term.

Observe: the 90 second daily scan

At the end of the day, write a single page scan. It takes 90 seconds if you keep to the format. Answer three prompts:

-

Money Moves: list each transaction you made today in one line. Include cash, card, transfers, and subscriptions triggered.

-

Mood Map: rate your emotional tone about money on a 1 to 10 scale and add one sentence explaining why.

-

Signal: one sentence describing a pattern you noticed. Example: I bought coffee twice this week when I felt behind on work.

This short ritual trains your attention and creates a dataset. Over two weeks your journal starts to look like a map of recurring micro-decisions.

Hypothesize: the experiment card

Every week, convert one Signal into an Experiment Card. The card is one sticky note or one line in your journal with four fields:

-

Hypothesis: If I [change X], then [expected outcome].

-

Measurement: how I will track it. Keep it numeric or binary.

-

Timebox: two weeks max.

-

Contingency: what I will do if it fails.

Example card: Hypothesis: If I delay nonessential online shopping until Saturday, I will reduce impulse purchases by 30 percent. Measurement: count impulse buys. Timebox: two weeks. Contingency: add a 24 hour cooling off rule.

This turns judgment into an experiment. You no longer feel like a failure when behavior persists. You are an investigator collecting evidence.

Iterate: the monthly synthesis

At the end of the month, synthesize. This is where clarity emerges. Use a single page with four sections:

-

Signal Summary: list recurring behaviors and percentages.

-

Wins and Losses: what improved and what regressed.

-

Redesign: one policy change for next month.

-

Intentional Delight: one small spend to celebrate progress.

If you follow the Observe and Hypothesize steps, the synthesis will be remarkably clear. You will see what habits consume your attention, where money supports your life, and where it gets in the way.

Unconventional tools that add rocket fuel

Journaling does not need to be purely pen and paper. Here are three out-of-the-box tools that make patterns pop.

The Emotion Ledger

Create two columns: Emotion and Expense. For each expense, tag the dominant emotion at the moment of purchase. Over time you will see clusters: boredom purchases, reward purchases, social anxiety purchases. Labeling emotional drivers turns implied motives into explicit data. That is how you gain financial clarity.

The Trigger Map

Make a flowchart for the week that links contexts to purchases. For example: Friday evening + friends + scrolling = takeaway. Map the most common routes and design breakpoints. A breakpoint could be: text a friend with a different plan or schedule a walk at 8 pm.

The Portfolio Storyboard

Instead of a static net worth line, create a storyboard where each asset or liability is a character with a short narrative. Example: Emergency Fund is “The Guardian” with mission, strengths, and vulnerabilities. Credit Card is “The Rocket” who helps take off but explodes if overloaded. Storytelling helps you calibrate emotion and strategy together.

Why narrative matters

Numbers are necessary but not sufficient. Stories drive behavior. Your money story is a set of beliefs about what you deserve, how the world treats you, and how risk feels. Journaling converts those beliefs into testable claims. When you write a narrative about a habit you can interrogate it: Is it true? Is it useful? What evidence would change this story?

Try this prompt once a month: Write a 200 word story called “A Day in the Life of My Money” from the perspective of your current top three financial commitments. Read the story aloud. Which character do you want to keep? Which do you want to fire?

Micro-rituals that shift identity

Identity shift is the hardest part of financial transformation. Micro-rituals help.

The Signoff Ritual

At the end of every purchase, write a one word note in your journal: why. Why did you buy this? This tiny act slows the autopilot and creates friction for impulse buys.

The Morning Ledger

Spend three minutes each morning reviewing yesterday’s 90 second scan. Confirm your priorities for today in one line. This primes your attention and reduces reactive spending.

The Quarterly Apology and Gratitude

Once each quarter, write a short apology to yourself and a gratitude list for where money served you. This balances discipline with compassion and prevents burnout. Explore more on how gratitude improves mental and financial health in our guide.

Case study: from anxiety to agency

Here is a condensed example of the method in action.

A reader named Lara started with chronic credit card anxiety. Her Observe logs revealed that late night shopping after stressful days at work led to most of her overspending. Her Experiment Card introduced a “buffer hour” after work where she swapped scrolling for a walk. Measurement showed impulse purchases dropped 55 percent. Her monthly synthesis redesigned her savings allocation to include a “comfort fund” so occasional small treats did not feel like betrayals. The emotional ledger revealed that many purchases were attempts at immediate comfort rather than long term satisfaction. With adjustments she regained control and reframed credit card use as a tool rather than a trap.

This is financial clarity in action. It is not about one-time budgeting wins. It is about transforming the system around your decisions.

Uncommon prompts that produce big insights

If you journal only the three daily prompts above you will already improve. But for deeper leaps, try these prompts once a week.

-

If I had to live on 80 percent of my current income for a year what would I cut first and what would I protect?

-

Which recurring payment exists to avoid a difficult conversation or task?

-

List three purchases you regret and write one sentence for each describing how you would decide differently now.

-

Describe your ideal day paid for entirely by passive income. What habits would that require?

These prompts force you to clarify trade offs and reveal hidden subscriptions and emotional anchors.

Technology and analog: a hybrid workflow

Use a cheap notebook for the daily 90 second scan and a simple digital tool for measurement. The tactile act of writing anchors memory. Spreadsheets are better for aggregating counts and trends. Sync the two: transcribe weekly totals into a simple spreadsheet and let the numbers accumulate. Treat the notebook as the creative lab, the spreadsheet as the evidence vault.

Common objections and how to handle them

I do not have time. The 90 second scan plus a weekly 5 minute card is less time than most people spend deciding what to eat for lunch. Time saved comes from fewer regret purchases and clearer priorities.

I am not disciplined. Experimentation reduces moral pressure. If an experiment fails you treat it as data, not proof of character. That is kinder and more effective.

I do not like writing. Use voice notes. Speak the 90 second scan into your phone. Transcribe if you want or keep audio files as your primary dataset.

A compounding framework

Journaling compounds like interest. The first month produces small wins. By month three you have a language for your financial life. By month six you can design policies that preempt common failure modes. The key is consistency plus curiosity. Keep the practice small enough to sustain and bold enough to challenge current narratives.

Journaling for Financial Clarity: Endnote experiment

Before you close this article, write one line now: What is one money habit you will test this week? Write it down. Make an Experiment Card. That single act is a micro-commitment that turns abstract insight into practical work.

Remember the title of this piece, Journaling for Financial Clarity: A Radical System for Money Mindset and Strategy. Keep that phrase as a tiny talisman. When you feel lost, return to it and to your journal. Over time you will notice not only improved balances but reduced noise and a clearer sense of who you are becoming with money.

Finally, one last affirmation to write in your journal tonight: I am an investigator of my financial life. Curiosity will guide me more than shame. Financial clarity will follow.

Journaling for Financial Clarity: A Radical System for Money Mindset and Strategy

Journaling for Financial Clarity: A Radical System for Money Mindset and Strategy

Journaling for Financial Clarity: A Radical System for Money Mindset and Strategy

Read more on Journaling for Financial Clarity